Learn the minimum credit score for home loan Australia, how lenders assess your profile, and how to improve your chances of approval.

What Credit Score Is Needed to Buy a House in Australia?

There is no single minimum credit score for home loan Australia. Lenders do not apply a universal cut-off; instead, they assess your entire financial position, including income, expenses, debts, and repayment history.

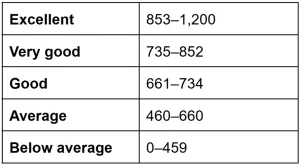

That said, credit score ranges provide a useful benchmark. According to Equifax, credit scores in Australia typically fall within the following bands:

Most mainstream lenders generally prefer borrowers with scores in the “good” range or higher. However, approval is still possible outside these ranges depending on your broader financial profile and the lender’s risk appetite.

Key Credit Score Guidelines in Australia

Understanding how your credit score is assessed can help you position yourself more effectively when applying for a home loan. Credit scores are calculated by agencies such as Equifax, Experian, and illion.

While scoring models differ slightly, lenders typically interpret scores using similar principles.

- Higher scores indicate lower risk and may improve access to competitive loan options

- Mid-range scores may still be acceptable but could limit lender choice

- Lower scores may require stronger supporting factors such as higher deposits or stable income

It is important to note that your credit score is only one part of the assessment. Lenders also evaluate serviceability, which includes your ability to meet repayments under different interest rate scenarios.

Important Considerations Beyond Credit Score

Focusing only on the minimum credit score for home loan Australia can be misleading. Lenders assess applications holistically, meaning other financial factors can carry equal or greater weight.

Key considerations include:

- Income stability and employment type

- Existing debts and financial commitments

- Savings history and deposit size

- Repayment behaviour across all credit accounts

For example, a borrower with a moderate credit score but strong income and low debt may be considered more favourably than someone with a high score but inconsistent financial behaviour.

What Is the Lowest Credit Score to Get a Mortgage?

There is no officially defined lowest credit score for mortgage approval in Australia. Some lenders may consider applications with lower scores, but these cases often involve additional conditions.

These conditions may include:

- Larger deposit requirements

- Fewer lender options

- More detailed documentation

- Potentially higher interest margins (subject to lender policy)

Because lending criteria vary, working with a mortgage broker can help identify lenders that are more flexible with credit history. This is particularly relevant for first home buyers who may not have an extensive credit record.

Can I Raise My Credit Score 100 Points in 30 Days?

Yes, it is possible to raise your credit score by 100 points in 30 days with the right strategies and dedication.

Improving your credit score is possible, but significant increases within a short timeframe are generally uncommon. Credit scores in Australia are based on historical financial behavior under the comprehensive credit reporting system.

According to Moneysmart, your score is influenced by repayment history, credit usage, and the number of credit applications. While correcting errors on your credit file or reducing outstanding balances may result in incremental improvements, meaningful changes typically occur over several months rather than weeks.

The most effective approach is to maintain consistent repayment behaviour, avoid multiple credit applications in a short period, and manage debt responsibly.

What Is the Biggest Killer of Credit Scores?

From a lender’s perspective, the most significant negative signals relate to repayment behaviour. Missed payments, defaults, and persistent arrears are among the strongest indicators of risk.

Other factors that can impact your credit score include:

- High levels of unsecured debt such as credit cards or personal loans

- Frequent credit applications within a short period

- Defaults or court judgments recorded on your credit file

Maintaining financial consistency is critical. Even small lapses, such as missed repayments, can have a disproportionate impact on your credit profile.

How to Find the Right Home Based on Your Credit Score Using a Mortgage Broker

Your credit score does not just influence whether you are approved for a loan. It also affects how much you can borrow and, ultimately, the type of property you can realistically purchase.

This is where a mortgage broker service becomes particularly valuable. A mortgage broker first home buyer works with can translate your credit profile into a practical borrowing range and match you with lenders that align with your situation.

A structured approach typically includes:

- Assessing your borrowing capacity based on your full financial profile

- Identifying lenders suited to your credit position

- Structuring your application to improve approval likelihood

- Aligning your property search with realistic financing outcomes

By combining credit insights with lender expertise, a broker helps ensure you are making decisions based on accurate and achievable parameters.

How Open Home Loans Supports First Home Buyers

If you are navigating the minimum credit score for home loan Australia and unsure where you stand, Open Home Loans provides a structured pathway forward.

Open Home Loans connects you with experienced mortgage specialists who guide you through every stage of the process. This includes assessing your credit position, identifying suitable lenders, and helping you understand your borrowing capacity.

What differentiates this approach is the integration of human expertise with digital tools. Rather than relying solely on manual research, relevant loan options are surfaced based on your financial profile, improving both clarity and efficiency.

You can explore tailored support for first home buyers here.

Taking the Next Step

Understanding your credit score is an important first step, but it should be part of a broader strategy. Reviewing your financial position, understanding lender expectations, and seeking guidance where needed can significantly improve your outcomes.

If you are considering your options, you can also estimate potential loan scenarios here.

FAQ: Minimum Credit Score for Home Loan Australia

What credit score is needed to buy a house in Australia?

There is no fixed minimum credit score. Most lenders prefer scores in the “good” range or higher, typically around 625+ on the Equifax scale, but approval depends on your full financial profile.

What is the lowest credit score to get a mortgage?

There is no universal minimum. Some lenders may accept lower scores, but this often involves stricter conditions such as larger deposits or reduced borrowing capacity.

Can I raise my credit score 100 points in 30 days?

Large increases in a short timeframe are uncommon. Improvements typically occur over several months through consistent repayment behaviour and responsible credit use.

What is the biggest killer of credit scores?

Missed repayments, defaults, and high levels of unsecured debt are among the most significant negative factors affecting credit scores.

Does a low credit score mean I cannot get a home loan?

Not necessarily. Some lenders specialise in borrowers with lower credit scores, but options may be more limited and subject to additional requirements.

How can a mortgage broker help with a low credit score?

A broker can identify lenders with more flexible criteria, structure your application effectively, and help align your borrowing expectations with your financial position.

Disclaimer

This article provides general information only and does not constitute financial advice. Loan suitability depends on individual circumstances, lender criteria, and regulatory requirements.

Sources

- Australian Securities and Investments Commission – Credit and lending regulations

- Equifax – Credit score ranges and methodology

- Moneysmart – Credit scores and home loan guidance

- Mortgage & Finance Association of Australia – Why choose a broker